Introduction

Using a credit card is common, but charge cards are another alternative. Charge cards and credit cards differ in several ways, with the monthly payment being critical. Consider the alarm on your watch. Using a credit card forces you to get out of your slumber—and pay off your balance. However, there is a "snooze button" on credit cards. If you cannot pay the entire debt at once, at least the minimum payment is required, and the balance can be paid off over time. Learn more about charge cards vs. credit cards by continuing.

What Is a Charge Card?

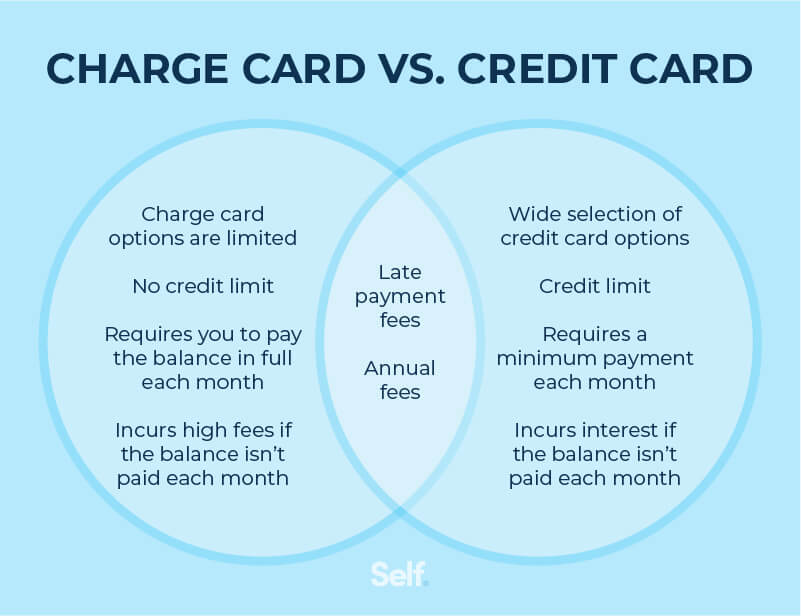

Essentially, a charge card functions similarly to a credit card. Instead of a fixed credit limit, however, purchases are authorized after careful examination of the customer's creditworthiness, including past purchases, payment history, and other factors. Users of charge cards must pay off their monthly balance in full. This means that, unlike credit cards, charge cards do not have a set minimum monthly payment or interest rate. However, late fees or interest may be applied if the balance is not paid monthly.

What Is a Credit Card?

You borrow money when you use a credit card. When you apply for a credit card, the issuing firm will set your credit limit or the maximum amount you can borrow from them. Each time you purchase with your credit card, you borrow money from the issuing bank and must repay a percentage of that amount every month. Some of the most common credit cards include Mastercard, Visa, and Discover.

What Are the Differences Between Charge Cards and Credit Cards?

The criteria above make credit cards vs. charge cards seem interchangeable; nonetheless, there are significant distinctions between the two in areas such as spending restrictions, billing cycles, and credit checks.

Spending Limit

In contrast to credit cards, charge cards often do not have spending limits. For the most part, charge cards do not have a predetermined credit limit, so you can spend freely without worrying about how your spending will affect your credit utilization ratio.

Payment Cycles

The balance on a charge card should be paid in full at the end of each billing cycle. If the bill isn't paid in full, the account could be terminated or a considerable penalty cost assessed. As opposed to debit cards, credit cards often only require a minimum payment each month and rollover balances into the next billing cycle. Even if you pay the minimum monthly, interest may still be charged beginning with the following billing period.

Late Fees

Charge cards have the exact potential costs of regular credit cards. There are, however, a few distinctions that should be made clear. If your monthly charge card amount isn't paid in whole by the due date, you may be charged a hefty late fee instead of interest. We may need to terminate or suspend your account if you incur too many late fees. Late fees on credit cards are typically less severe than those on other payment types and can sometimes be avoided entirely. In addition, you can avoid incurring any additional fees by paying at least the minimum amount due each month on your credit card.

Rewards and Perks

Although charge cards have long held the reputation of being the best rewards cards due to their exclusive benefits, credit card companies have been boosting the value of their rewards programs in recent years. Compared to American Express charge cards vs. credit cards option, the Chase Sapphire Preferred Card, for instance, fares quite well. However, the best incentives and bonuses still tend to be found on charge cards, especially for individuals who frequently travel. Because of their revolving nature, charge cards present a fantastic opportunity to rack up frequent flyer miles and points.

Credit Inquiries

Soft inquiries, also known as soft credit checks, occur when you or a third party, with your permission, view your credit report independently of any specific application. Inquiries considered "soft" do not affect a credit report. Applying for a charge or credit card will result in a hard inquiry. In the case of credit cards, a hard inquiry lets issuers evaluate applicants and set spending limits. Credit scores may be affected by hard inquiries made to a credit report for up to two years.

Conclusion

Depending on the card, charge and credit card holders may be eligible to earn rewards and points for making purchases. However, charge cards usually do not have a spending restriction and require monthly bill payments. Credit cards have spending limits, required minimum payments, and a balance transfer option. Charge cards are a good option for consumers with excellent credit and the means to pay off their balance in full each month. Using one of these cards can let you reap the benefits of rewards without breaking the bank. If you'd like more freedom with your card, a credit card might be more suitable.