Introduction

Your house is more than just a place to sleep and a financial haven. Indeed, it entails both of these and much besides. If you need quick money for unexpected expenses like car repairs, house renovations, or even tuition, you may continuously tap into the equity you've built up in your property. Mortgage refinancing is one option for getting the money you've put into your home back into circulation. Cash-out refinancing and home equity loans are two of the most popular. With cash-out refinancing, you exchange your current mortgage for a new one, presumably with a more favourable interest rate. A home equity loan is a second mortgage that allows you to borrow money against the value of your home. Here is a guide about comparing Home Equity Loan vs. Refinance.

What's the Difference Between a Home Equity Loan and a Refinance?

Mortgage Position

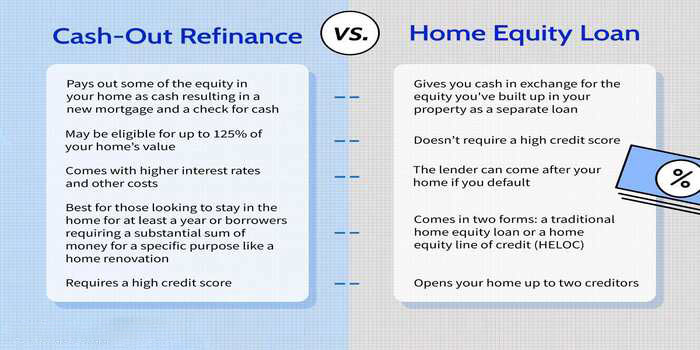

Equity in your property can be used as collateral for a loan. The funds are yours to use as you see fit, whether to fix up or renovate your home, pay for school, medical bills, etc. A home equity loan can be considered a second, smaller mortgage. A refinance is not a second mortgage like a home equity loan. You might think of it as a replacement for your current mortgage. Refinancing into a loan with a longer term or a cheaper interest rate might reduce your monthly payment, and total interest paid. The ability to refinance from an adjustable to a fixed-rate mortgage can help you lock in a cheaper interest rate for the long haul.

Consolidating debts with higher interest rates is one possible use for a refinance. Refinancing your mortgage allows you to consolidate high-interest debt, such as credit card and personal loan balances, into one low monthly payment. A cash-out could save you a lot of interest payments, given that mortgage rates are often lower than credit card and vehicle loan rates.

Costs

As a second lien loan, home equity loans often carry higher interest rates than first mortgages or refinance loans. The mortgagee (the original lender) gets priority over the second mortgagee (the home equity lender) if you default on your payments. This increases the danger associated with taking out a home equity loan. For this reason, lenders prefer interest rates that are slightly higher to mitigate risk.

Qualifying

Since a refinancing loan is a first-lien loan, it is typically easier to get approved. In the event of a loan default, the lender would have a priority claim on the collateral. Although the interest rate on a new loan will likely be lower than that of a home equity line of credit, it may not be significantly cheaper. These days' typical loan rates can be obtained from Freddie Mac. Additionally, you should verify the terms of your present mortgage to ascertain whether or not a prepayment penalty applies. If so, settling it before pursuing a refinance could be necessary. Inquire if the cost can be removed if you refinance with your current mortgage servicer instead of switching to a different business.

How Home Equity Loans Work

Home equity loans function similarly to primary mortgages because that is essentially what they are. Select a lending institution, fill out an application, submit your paperwork, wait for approval, and finalise the loan closing. The loan amount will be sent to you in a lump sum, and you will make payments on it every month, just like you did with your first mortgage.

How Refinances Work

A refinance eliminates the need for a second mortgage payment but modifies the existing mortgage payment because the new loan pays down the old one. It's possible that your new monthly payment could be greater than your mortgage or cheaper, depending on your credit history, the loan term you choose, and the total amount you borrow.

Conclusion

Homeowners who wish to access the equity they've built in their houses through cash-out refinancing or a home equity loan have options. Whether you should refinance or take out a home equity loan depends on several factors, including your equity position, the intended use of the funds, and the anticipated length of time in the house. Home refinancing and home equity loans can offer potential financial advantages. Think about your goals, preferred repayment schedule, expected length of time in the place, and the amount of equity you currently have in the home to help you decide which path is best for your family. Rates and closing expenses can vary substantially from one lender to the next, so it pays to shop around.