Introduction

Thrifts vs. banks: What’s the difference? The primary distinction between banks and thrift institutions is that banks cater to the needs of both businesses and individuals. Thrifts, conversely, cater to individual customers rather than commercial enterprises. Typically, a bank will receive a federal or state government charter. On the other hand, a thrift charter comes from either the state's department of financial regulation or the federal government's office of thrift supervision.

What is a Bank?

Any business making loans and accepting deposits is considered a bank. The stability and expansion of a nation's economy rely heavily on its banking system. Financial institutions also provide access to credit through the capital markets, either directly or indirectly. Higher authorities typically enforce banking regulations.

What is Thrift?

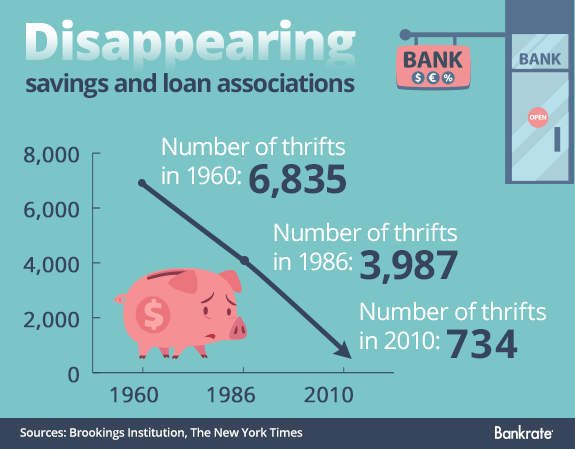

The term "thrift" describes a bank that relies heavily on public savings for its funding. Thrift provides several different types of cooperative banking structures. Financial institutions such as credit unions, mutual savings banks, and savings and loan associations are a few examples. Thrifts have larger savings accounts but fewer loan options. Facilities provided by thrift banks are varied. The services provided to customers include the more commonplace ones such as savings accounts, bank accounts, mortgage loans, unsecured loans, and charge cards.

Differences Between Thrift and Bank

We have drawn a detailed comparison between banks vs thrifts below:

Limitation to Offer Products

Traditional banks cater to people and businesses, but thrift institutions focus solely on the latter. Additionally, a thrift bank's portfolio must consist of consumer loans for at least 65% of the bank's total loans. In addition, they can only lend 50% of their total assets to smaller businesses, while 20% goes to commercial loans. No such regulations apply to commercial banks.

Higher Yield and Liquidity

In contrast to commercial banks, Thrift institutions can often obtain cheap money through Federal Home Loan Banks at a low-interest rate. They can now offer their savers a better return on their money. In addition, their liquidity is far higher than that of traditional banks, making it possible for them to provide mortgage loans for homes.

Range of Products

Accounts for managing wealth, participating in insurance programs, exchanging currency, etc., are just some of the services banks offer. The general people can choose from various products to help them achieve their monetary objectives. Typical banks offer a wide range of services, making them convenient one-stop shops for banking needs. On the other hand, Thrift banks limit their customers to a small selection of accounts, and their products are straightforward and easy to maintain.

Regulation

In the 1850s, the federal government of the United States authorized the creation of thrift institutions. As a result, they are subject to stricter rules than traditional banks. They are especially vulnerable to a housing market slump because they are mandated by law to have at least 65% of their mortgage lending. On the other hand, they proved pretty resilient during the 2008 credit crisis because they were shielded from the commercial banks' debt. For this reason, they fared better than more traditional banks during the crisis.

Charter

Commercial banks must obtain their charter from either the federal or state government. Stockholders of the bank can make the call based on the best interest of the company as a whole and its future growth. The national bank charters are issued by the United States Department of the Treasury's Office of the Comptroller of the Currency. Commercial banks can switch from a state to a federal charter in the United States.

Ownership

A depositor, a borrower, or shareholders who own most of the S&''L's charter stock are the usual people who start a thrift bank, one of two types of savings and loan associations that can be founded. Another name for it is "dual ownership." But banks operate as businesses that provide their services on a national or regional scale and are governed by a board of directors elected by the shareholders. Therefore, depositors and borrowers are only able to own traditional banks jointly.

Conclusion

Thus, there are several distinctions between thrifts vs banks. Banks can make money in a few different ways. Interest, transaction fees, and professional financial counseling are a few examples. On the other hand, Thrift stores offer customers an abundance of options. More rules apply to thrifts than to banks. Banks provide several retail provisions. Examples include credit cards, debit cards, mortgages, unsecured personal loans, instant demand deposits, automated teller machines, NEFT, and reloadable prepaid cards. On the other hand, Thrift stores only offer a few services to their customers. Overall, financial institutions like banks and thrifts are different in significant ways.