Introduction

What are guarantor loans? Guarantor loans allow people with low credit scores to borrow money from a financial institution by providing a cosigner. A "guarantor" promises to pay your bills if you can't. A guaranteed loan may be a smart alternative for you if you start in life and still need a solid credit history. Alternatively, you may have a history of credit mismanagement, such as late payments, account defaults, or an excessive number of credit applications. You can improve your credit history with a guarantor loan if you make your payments on time.

Types of Guarantors

A guarantor could be helpful in a wide variety of contexts. Both examples are helping folks with low incomes or poor credit records. Moreover, guarantors must avoid assuming complete financial responsibility for the guaranteed obligation. The following are examples of when a guarantor is required and the many types of guarantors that may be involved.

Guarantors as Certifiers

Guarantors can play a role in someone's life in many ways, including pledging their assets as collateral against loans, facilitating employment, and facilitating travel documents. In these cases, guarantors attest to the applicant's familiarity with them and verify their identities by inspecting their government-issued picture identification.

Limited Vs. Unlimited

A guarantor's obligations and role in the loan's repayment may be time- and money-bound, depending on the loan arrangement's terms. For instance, a limited guarantor might be asked to back a loan for a set time before the entire burden of repayment and the repercussions of default fall solely on the borrower. A restricted guarantor can be accountable for backing only a minimal loan sum. In contrast, limitless guarantors will be held responsible for the entire loan amount for the entirety of the loan's term.

Other Contexts for Guarantors

Borrowers with weak credit are just some who turn to guarantors. Landlords often ask for lease guarantors from tenants renting for the first time. Students at universities often have their parents sign as guarantors in case they default on rent payments or terminate the lease early.

Guarantors Vs. Cosigners

A cosigner is someone whose name appears on the asset's title with the borrower. In contrast, a guarantor guarantees the loan or other obligation. When a borrower's salary needs to be higher to meet the lender's requirements, they may need to work out a cosigner agreement. On the other hand, guarantors help out even if the borrower has good income but bad credit. The difference between a guarantee and a cosigner is that a guarantor has no legal right to the collateral.

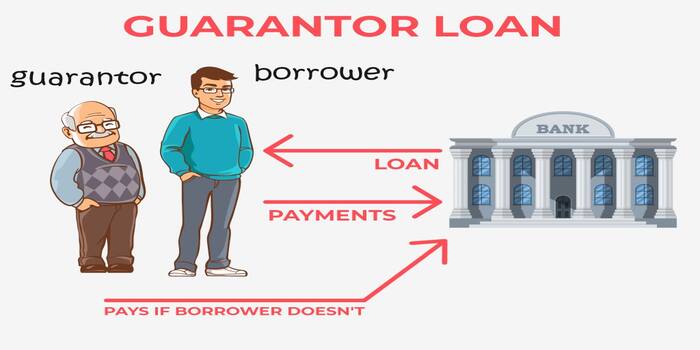

How Do Guarantor Loans Work?

How do guarantor loans work? Like any other loan, a guarantor loan requires borrowing money from a lender and making regular payments toward paying off the loan. With a guarantor, however, a third party has agreed to cover your payments if you cannot. Depending on the lending institution, the guarantor may first be the loan recipient. They have two weeks to reconsider their decision to give it to the borrower or return it to the lender. Assuming the agreement is satisfactory to the guarantor, you will receive a lump sum payment. You must repay the loan following its terms, usually between one and seven years.

What Are the Risks of a Guarantor Loan?

Remember that guarantor loans typically have higher interest rates than other lending options. If you're considering taking out a loan, think carefully about whether or not you need it and whether or not you can afford the monthly payments. Aside from that, the danger is minimal. Your guarantor takes on more risk because they will be responsible for making the payments in your place if you cannot. Before agreeing to guarantee someone else's loan, it's wise to educate oneself about the responsibilities and potential consequences of taking on this role.

Conclusion

A guarantor is someone who promises to cover the debt of another person in the case that the debtor cannot. While not a signatory to the deal itself, a guarantor provides the lender with some peace of mind. If a guarantor agrees to back your loan, they should be able to prove that they have good credit and can afford the payments. For the borrower, having a guarantee on the loan agreement is helpful. It speeds up the approval process for a deal and, in many cases, increases the dollar amount. The guarantor assumes liability in the event of a default by the borrower. Legal action can be taken if they still need to pay the outstanding balance. Their credit rating will suffer as a result as well.